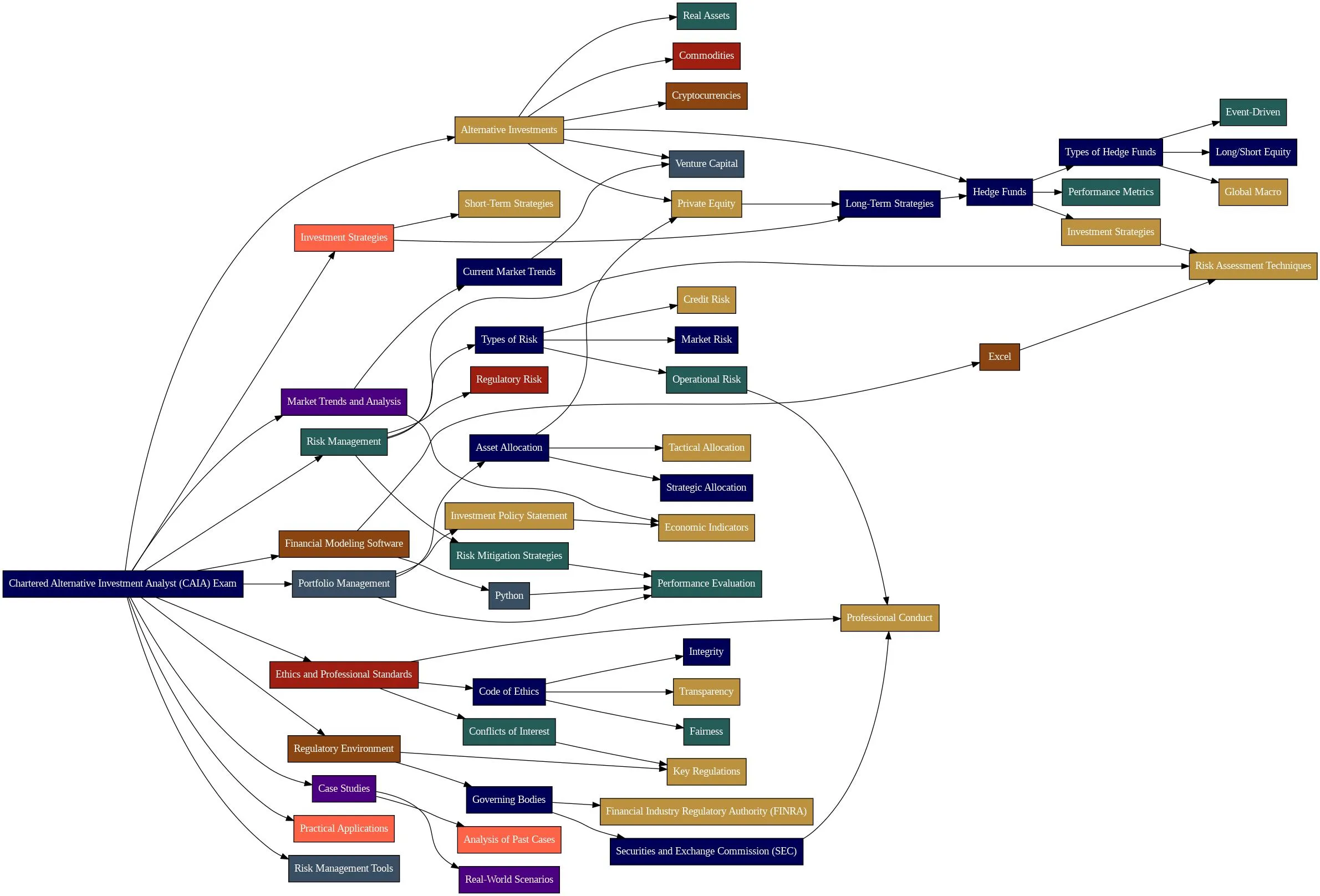

Quiz-summary

0 of 30 questions completed

Questions:

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10

- 11

- 12

- 13

- 14

- 15

- 16

- 17

- 18

- 19

- 20

- 21

- 22

- 23

- 24

- 25

- 26

- 27

- 28

- 29

- 30

Information

Premium Practice Questions

You have already completed the quiz before. Hence you can not start it again.

Quiz is loading...

You must sign in or sign up to start the quiz.

You have to finish following quiz, to start this quiz:

Results

0 of 30 questions answered correctly

Your time:

Time has elapsed

Categories

- Not categorized 0%

- 1

- 2

- 3

- 4

- 5

- 6

- 7

- 8

- 9

- 10

- 11

- 12

- 13

- 14

- 15

- 16

- 17

- 18

- 19

- 20

- 21

- 22

- 23

- 24

- 25

- 26

- 27

- 28

- 29

- 30

- Answered

- Review

-

Question 1 of 30

1. Question

When managing a portfolio that includes a significant exposure to a particular corporate issuer’s debt, and the portfolio manager anticipates a potential deterioration in the issuer’s credit quality, which of the following derivative instruments would be most appropriate for hedging this specific credit risk?

Correct

This question tests the understanding of credit default swaps (CDS) and their role in managing credit risk. A CDS is an insurance-like contract where the buyer makes periodic payments to the seller in exchange for protection against a credit event. If a credit event occurs (e.g., default, bankruptcy), the seller compensates the buyer. In this scenario, the fund manager is concerned about the creditworthiness of a specific corporate bond issuer. By purchasing a CDS on that issuer’s debt, the fund manager is effectively hedging against the risk of default. The periodic payments made are the premium for this protection. The other options are incorrect because selling a CDS would expose the fund to the credit risk, buying a credit-linked note is a different instrument, and investing in a diversified portfolio, while good practice, doesn’t directly address the specific credit risk of the targeted issuer in the way a CDS does.

Incorrect

This question tests the understanding of credit default swaps (CDS) and their role in managing credit risk. A CDS is an insurance-like contract where the buyer makes periodic payments to the seller in exchange for protection against a credit event. If a credit event occurs (e.g., default, bankruptcy), the seller compensates the buyer. In this scenario, the fund manager is concerned about the creditworthiness of a specific corporate bond issuer. By purchasing a CDS on that issuer’s debt, the fund manager is effectively hedging against the risk of default. The periodic payments made are the premium for this protection. The other options are incorrect because selling a CDS would expose the fund to the credit risk, buying a credit-linked note is a different instrument, and investing in a diversified portfolio, while good practice, doesn’t directly address the specific credit risk of the targeted issuer in the way a CDS does.

-

Question 2 of 30

2. Question

When evaluating a hedge fund’s offering document, an investor encounters a statement detailing the investment objective as “investing in all global markets with the aim of maximizing returns through any available strategy, without reference to any specific market index.” From a CAIA perspective, what is the primary deficiency of this disclosure?

Correct

The CAIA Level I curriculum emphasizes the importance of clear and informative disclosure for hedge fund investors. A well-defined investment objective should specify the markets of operation, the general investment strategy, and a relevant benchmark. The first example provided in the text describes an investment universe that is “every market known to exist,” a strategy of “capital appreciation,” and “no effective benchmark.” This broad and unspecific language fails to provide investors with a clear understanding of the fund’s activities and risks, making it difficult to assess its suitability. In contrast, the second example offers a concise and informative statement that addresses all three key aspects of an investment objective, allowing investors to make informed decisions.

Incorrect

The CAIA Level I curriculum emphasizes the importance of clear and informative disclosure for hedge fund investors. A well-defined investment objective should specify the markets of operation, the general investment strategy, and a relevant benchmark. The first example provided in the text describes an investment universe that is “every market known to exist,” a strategy of “capital appreciation,” and “no effective benchmark.” This broad and unspecific language fails to provide investors with a clear understanding of the fund’s activities and risks, making it difficult to assess its suitability. In contrast, the second example offers a concise and informative statement that addresses all three key aspects of an investment objective, allowing investors to make informed decisions.

-

Question 3 of 30

3. Question

When evaluating the potential inclusion of a fund of hedge funds (FoF) into an existing equity portfolio, an investment manager needs to determine if the FoF offers a superior risk-adjusted return compared to the portfolio’s current risk-return profile. Using the Sharpe ratio concept adapted for portfolio integration, the manager calculates a ‘hurdle rate’ for the FoF. This hurdle rate represents the minimum expected return the FoF must achieve to justify its inclusion, considering its volatility and its correlation with the existing portfolio. Given the following data: the risk-free rate (Rf) is 3.90%, the expected return of the existing portfolio (Rp) is 9.92%, the volatility of the existing portfolio (σp) is 13.98%, the expected return of the FoF (Rh) is 8.97%, the volatility of the FoF (σh) is 5.78%, and the correlation between the FoF and the portfolio (ρh,p) is 0.47. What is the calculated hurdle rate for the FoF, and does it represent a valuable addition for risk budgeting purposes?

Correct

The question tests the understanding of how to determine if a new asset class, in this case, a fund of hedge funds (FoF), adds value to an existing portfolio from a risk budgeting perspective. The core concept is that a new asset should be added if its risk-adjusted return, relative to its correlation with the existing portfolio, exceeds that of the existing portfolio. Equation 11.1 from the provided text outlines this principle. The hurdle rate represents the minimum required return for the new asset to be considered a valuable addition. This hurdle rate is calculated by adjusting the portfolio’s excess return by the ratio of the new asset’s volatility to the portfolio’s volatility, and then scaling this by the correlation between the new asset and the portfolio. The formula for the hurdle rate is: Hurdle Rate = Rf + (Rp – Rf) * (σh / σp) * ρh,p. Substituting the given values: Rf = 3.90%, Rp = 9.92%, σh = 5.78%, σp = 13.98%, and ρh,p = 0.47. Hurdle Rate = 0.0390 + (0.0992 – 0.0390) * (0.0578 / 0.1398) * 0.47 = 0.0390 + (0.0602) * (0.4134) * 0.47 = 0.0390 + 0.0117 = 0.0507, or 5.07%. Since the expected return of the FoF (8.97%) is greater than this hurdle rate, it is considered a valuable addition for risk budgeting.

Incorrect

The question tests the understanding of how to determine if a new asset class, in this case, a fund of hedge funds (FoF), adds value to an existing portfolio from a risk budgeting perspective. The core concept is that a new asset should be added if its risk-adjusted return, relative to its correlation with the existing portfolio, exceeds that of the existing portfolio. Equation 11.1 from the provided text outlines this principle. The hurdle rate represents the minimum required return for the new asset to be considered a valuable addition. This hurdle rate is calculated by adjusting the portfolio’s excess return by the ratio of the new asset’s volatility to the portfolio’s volatility, and then scaling this by the correlation between the new asset and the portfolio. The formula for the hurdle rate is: Hurdle Rate = Rf + (Rp – Rf) * (σh / σp) * ρh,p. Substituting the given values: Rf = 3.90%, Rp = 9.92%, σh = 5.78%, σp = 13.98%, and ρh,p = 0.47. Hurdle Rate = 0.0390 + (0.0992 – 0.0390) * (0.0578 / 0.1398) * 0.47 = 0.0390 + (0.0602) * (0.4134) * 0.47 = 0.0390 + 0.0117 = 0.0507, or 5.07%. Since the expected return of the FoF (8.97%) is greater than this hurdle rate, it is considered a valuable addition for risk budgeting.

-

Question 4 of 30

4. Question

During a comprehensive review of a process that needs improvement, a large aerospace manufacturer, Boeing, identifies a persistent exposure to price volatility for a critical raw material, aluminum. While direct negotiations with aluminum producers are sometimes possible, the timing of Boeing’s demand often creates short-term imbalances, exposing the company to price fluctuations. In this context, how do market participants, such as speculators, typically facilitate the management of this price risk, particularly when the futures market for aluminum exhibits an upward-sloping price curve (contango)?

Correct

The scenario describes a situation where a manufacturer, Boeing, needs aluminum for its production cycle, which may not align with the availability from producers. Boeing faces price risk due to potential fluctuations in aluminum prices. Speculators play a crucial role by taking on this risk. In a contango market, the futures price (FT) is greater than the expected future spot price (E(ST)). This means speculators are willing to sell futures contracts at a price higher than what they anticipate the spot price to be at maturity. They do this because they expect to profit from the difference (FT – E(ST)) if the inequality holds. Boeing, as the hedger, is willing to pay this premium to eliminate the uncertainty of future aluminum costs. The question tests the understanding of why speculators are necessary in commodity markets and the conditions under which they operate, specifically relating to contango markets where they are compensated for taking on price risk.

Incorrect

The scenario describes a situation where a manufacturer, Boeing, needs aluminum for its production cycle, which may not align with the availability from producers. Boeing faces price risk due to potential fluctuations in aluminum prices. Speculators play a crucial role by taking on this risk. In a contango market, the futures price (FT) is greater than the expected future spot price (E(ST)). This means speculators are willing to sell futures contracts at a price higher than what they anticipate the spot price to be at maturity. They do this because they expect to profit from the difference (FT – E(ST)) if the inequality holds. Boeing, as the hedger, is willing to pay this premium to eliminate the uncertainty of future aluminum costs. The question tests the understanding of why speculators are necessary in commodity markets and the conditions under which they operate, specifically relating to contango markets where they are compensated for taking on price risk.

-

Question 5 of 30

5. Question

During a comprehensive review of a process that needs improvement, a financial institution is examining its strategies for managing non-performing loans. One of its divisions has been actively purchasing distressed debt from other financial entities that are eager to offload these assets to improve their balance sheets. The purchasing division’s strategy involves acquiring this debt at a substantial discount, with the expectation of either a recovery in the company’s fortunes or a conversion to equity. This activity is particularly valuable when other creditors, lacking the specialized expertise or risk appetite for a prolonged workout period, wish to exit their positions quickly. Which of the following best characterizes the role of the purchasing division in this context?

Correct

The scenario describes a situation where a distressed debt investor, often termed a ‘vulture investor,’ acquires debt from a company in financial distress at a significant discount. The core strategy of such investors is to profit from the potential recovery of the company or by converting the debt into an equity stake. The text explicitly states that distressed debt investors may help impatient creditors to cut their losses and remove bad debt from their books, receiving the distressed debt in return. This action is a form of facilitating the sale of distressed assets, allowing the original creditor to exit the position, which aligns with the role of a distressed debt buyer acting as a liquidity provider for other creditors.

Incorrect

The scenario describes a situation where a distressed debt investor, often termed a ‘vulture investor,’ acquires debt from a company in financial distress at a significant discount. The core strategy of such investors is to profit from the potential recovery of the company or by converting the debt into an equity stake. The text explicitly states that distressed debt investors may help impatient creditors to cut their losses and remove bad debt from their books, receiving the distressed debt in return. This action is a form of facilitating the sale of distressed assets, allowing the original creditor to exit the position, which aligns with the role of a distressed debt buyer acting as a liquidity provider for other creditors.

-

Question 6 of 30

6. Question

When evaluating the potential for value creation in alternative investment strategies, which of the following best describes the role of the transfer coefficient (TC) in relation to the Fundamental Law of Active Management?

Correct

The Fundamental Law of Active Management (FLAM) posits that the information coefficient (IC) and the breadth of the portfolio are the primary drivers of active return. The transfer coefficient (TC) is a factor that can erode the potential benefits of active management, even in alternative strategies. While alternative managers often benefit from fewer constraints, allowing for concentrated portfolios and market-neutral strategies, the costs associated with these techniques, such as borrowing costs for shorting, directly impact the TC. Therefore, even with a high IC, the TC must be considered as it quantifies the extent to which the gross active return can be translated into net active return after accounting for these costs. A low TC signifies that a significant portion of the potential active return is lost due to transaction costs and other frictions.

Incorrect

The Fundamental Law of Active Management (FLAM) posits that the information coefficient (IC) and the breadth of the portfolio are the primary drivers of active return. The transfer coefficient (TC) is a factor that can erode the potential benefits of active management, even in alternative strategies. While alternative managers often benefit from fewer constraints, allowing for concentrated portfolios and market-neutral strategies, the costs associated with these techniques, such as borrowing costs for shorting, directly impact the TC. Therefore, even with a high IC, the TC must be considered as it quantifies the extent to which the gross active return can be translated into net active return after accounting for these costs. A low TC signifies that a significant portion of the potential active return is lost due to transaction costs and other frictions.

-

Question 7 of 30

7. Question

During a period of rising inflation expectations, an investor observes that commodity futures prices are appreciating significantly. Based on the provided analysis, what is the most likely concurrent movement observed in the prices of equities and corporate bonds, and why?

Correct

The provided text highlights that commodity futures prices are positively correlated with changes in the inflation rate, while capital assets like stocks and bonds are negatively correlated. This is because rising inflation often leads investors to revise expectations of future inflation upwards, which negatively impacts the present value of future cash flows for stocks and bonds. Conversely, commodities are seen as a hedge against inflation, and their prices tend to rise with increasing inflation expectations. The text also notes that commodities are more sensitive to current economic conditions, whereas stocks and bonds are more influenced by long-term expectations. Therefore, when inflation expectations rise, commodity prices are expected to increase, while stock and bond prices are expected to decrease.

Incorrect

The provided text highlights that commodity futures prices are positively correlated with changes in the inflation rate, while capital assets like stocks and bonds are negatively correlated. This is because rising inflation often leads investors to revise expectations of future inflation upwards, which negatively impacts the present value of future cash flows for stocks and bonds. Conversely, commodities are seen as a hedge against inflation, and their prices tend to rise with increasing inflation expectations. The text also notes that commodities are more sensitive to current economic conditions, whereas stocks and bonds are more influenced by long-term expectations. Therefore, when inflation expectations rise, commodity prices are expected to increase, while stock and bond prices are expected to decrease.

-

Question 8 of 30

8. Question

During a comprehensive review of a leveraged buyout financing structure, a senior bank lender expresses concern about the overall risk profile. To mitigate their exposure, the bank insists on the inclusion of a significant tranche of capital that ranks below their own debt but above the equity in the capital stack. What is the primary regulatory or structural rationale behind the bank’s insistence on this specific type of subordinated financing?

Correct

The scenario describes a situation where a private equity firm is financing a leveraged buyout (LBO). Bank lenders, while providing senior debt, often require a layer of subordinated or junior debt below their own loans to mitigate their risk in case of default. This junior debt acts as a ‘loss tranche’ that absorbs initial losses before the senior lenders are impacted. Mezzanine debt, by its nature, is typically subordinated to senior bank debt and is therefore attractive to senior lenders as it increases their security. The question tests the understanding of why senior lenders would insist on mezzanine financing in an LBO structure, which is to enhance their own position by having a cushion of junior capital.

Incorrect

The scenario describes a situation where a private equity firm is financing a leveraged buyout (LBO). Bank lenders, while providing senior debt, often require a layer of subordinated or junior debt below their own loans to mitigate their risk in case of default. This junior debt acts as a ‘loss tranche’ that absorbs initial losses before the senior lenders are impacted. Mezzanine debt, by its nature, is typically subordinated to senior bank debt and is therefore attractive to senior lenders as it increases their security. The question tests the understanding of why senior lenders would insist on mezzanine financing in an LBO structure, which is to enhance their own position by having a cushion of junior capital.

-

Question 9 of 30

9. Question

During a period characterized by sharp, unpredictable price swings across multiple commodity markets, a portfolio manager employing a systematic trend-following strategy observes a significant decline in the strategy’s profitability. The manager attributes this underperformance primarily to the increased frequency of trades that are quickly reversed shortly after initiation. Which of the following best describes the phenomenon impacting the managed futures strategy?

Correct

This question tests the understanding of how managed futures strategies, specifically trend-following, are impacted by market volatility and the concept of ‘whipsaws’. A whipsaw occurs when a market trend reverses shortly after a position is established, leading to a series of small losses. In a highly volatile market with frequent trend reversals, a trend-following strategy is likely to experience more whipsaws. This leads to a higher frequency of trades and potentially increased transaction costs and slippage, eroding overall performance. While volatility can present opportunities, the core mechanism of trend-following is disrupted by rapid, unpredictable price swings, making it more susceptible to whipsaws and thus reducing its effectiveness in such environments.

Incorrect

This question tests the understanding of how managed futures strategies, specifically trend-following, are impacted by market volatility and the concept of ‘whipsaws’. A whipsaw occurs when a market trend reverses shortly after a position is established, leading to a series of small losses. In a highly volatile market with frequent trend reversals, a trend-following strategy is likely to experience more whipsaws. This leads to a higher frequency of trades and potentially increased transaction costs and slippage, eroding overall performance. While volatility can present opportunities, the core mechanism of trend-following is disrupted by rapid, unpredictable price swings, making it more susceptible to whipsaws and thus reducing its effectiveness in such environments.

-

Question 10 of 30

10. Question

When analyzing the cross-sectional distribution of real estate property returns for a given year, which segment of the distribution is most indicative of the return expectations for an opportunistic real estate investment strategy, reflecting its higher risk and potential for significant upside?

Correct

The question tests the understanding of how different real estate investment strategies are categorized based on their expected return profiles, specifically using the percentile ranges derived from a cross-sectional return distribution. Opportunistic real estate is characterized by investments that fall into the extreme tails of the return distribution, representing the highest potential returns and highest potential losses. According to the provided text, these are represented by the zero to 5th percentile and the 95th to 100th percentile ranges. Value-added investments fall into the ranges between the 5th and 25th percentiles (initially, due to repositioning efforts) and the 75th and 95th percentiles (after successful repositioning). Core investments are typically associated with the median return and the range between the 25th and 75th percentiles. Therefore, the highest potential returns, indicative of opportunistic strategies, are found in the upper tail of the distribution, specifically the 95th to 100th percentile.

Incorrect

The question tests the understanding of how different real estate investment strategies are categorized based on their expected return profiles, specifically using the percentile ranges derived from a cross-sectional return distribution. Opportunistic real estate is characterized by investments that fall into the extreme tails of the return distribution, representing the highest potential returns and highest potential losses. According to the provided text, these are represented by the zero to 5th percentile and the 95th to 100th percentile ranges. Value-added investments fall into the ranges between the 5th and 25th percentiles (initially, due to repositioning efforts) and the 75th and 95th percentiles (after successful repositioning). Core investments are typically associated with the median return and the range between the 25th and 75th percentiles. Therefore, the highest potential returns, indicative of opportunistic strategies, are found in the upper tail of the distribution, specifically the 95th to 100th percentile.

-

Question 11 of 30

11. Question

During a comprehensive review of a process that needs improvement, a group of private equity firms is considering a joint acquisition of a major corporation. Each firm individually possesses substantial capital, but the target company’s valuation exceeds the typical investment limit for any single firm, as stipulated by their respective fund agreements which cap single-deal exposure at 25% of total committed capital. Furthermore, the extensive due diligence required for such a significant transaction presents a considerable cost burden. Which of the following structures would best facilitate this acquisition while addressing these challenges?

Correct

The scenario describes a situation where multiple private equity firms are pooling resources to acquire a large company. This collaborative approach, known as a club deal, is often employed when a single firm lacks sufficient capital or is restricted by its limited partnership agreement from investing a large portion of its capital in one transaction. Club deals also allow for the sharing of due diligence costs and provide a mechanism for firms to gain a second opinion on the valuation of the target company. While the text mentions potential drawbacks like unclear leadership and decision-making, the primary drivers for engaging in club deals are the ability to participate in larger transactions and manage capital allocation constraints.

Incorrect

The scenario describes a situation where multiple private equity firms are pooling resources to acquire a large company. This collaborative approach, known as a club deal, is often employed when a single firm lacks sufficient capital or is restricted by its limited partnership agreement from investing a large portion of its capital in one transaction. Club deals also allow for the sharing of due diligence costs and provide a mechanism for firms to gain a second opinion on the valuation of the target company. While the text mentions potential drawbacks like unclear leadership and decision-making, the primary drivers for engaging in club deals are the ability to participate in larger transactions and manage capital allocation constraints.

-

Question 12 of 30

12. Question

During a comprehensive review of a portfolio’s historical performance, an analyst is examining a dataset of equity long/short hedge fund returns. The dataset represents the entire population of funds for a specific period. The calculated mean return for this population is 6.03%, and the second moment of the return distribution is 1.208%. Based on these figures, what is the population variance of the hedge fund returns?

Correct

The question tests the understanding of how to calculate the variance of a population of returns. The provided text defines variance using two formulas: E[X^2] – (E[X])^2 and the summation of (Xi – E[X])^2 / N. The scenario provides the mean return (E[X]) as 6.03% and the second moment (E[X^2]) as 1.208%. To calculate the variance, we use the formula Variance = E[X^2] – (E[X])^2. Plugging in the values: Variance = 1.208% – (6.03%)^2. It’s crucial to convert percentages to decimals for calculation: 0.01208 – (0.0603)^2 = 0.01208 – 0.00363609 = 0.00844391. Converting back to a percentage, this is approximately 0.844%. The other options are derived from incorrect calculations or misinterpretations of the formulas. Option B uses the standard deviation formula incorrectly. Option C incorrectly squares the second moment. Option D uses the sample variance formula (dividing by N-1) which is not applicable here as the data represents the entire population of hedge fund returns presented.

Incorrect

The question tests the understanding of how to calculate the variance of a population of returns. The provided text defines variance using two formulas: E[X^2] – (E[X])^2 and the summation of (Xi – E[X])^2 / N. The scenario provides the mean return (E[X]) as 6.03% and the second moment (E[X^2]) as 1.208%. To calculate the variance, we use the formula Variance = E[X^2] – (E[X])^2. Plugging in the values: Variance = 1.208% – (6.03%)^2. It’s crucial to convert percentages to decimals for calculation: 0.01208 – (0.0603)^2 = 0.01208 – 0.00363609 = 0.00844391. Converting back to a percentage, this is approximately 0.844%. The other options are derived from incorrect calculations or misinterpretations of the formulas. Option B uses the standard deviation formula incorrectly. Option C incorrectly squares the second moment. Option D uses the sample variance formula (dividing by N-1) which is not applicable here as the data represents the entire population of hedge fund returns presented.

-

Question 13 of 30

13. Question

When constructing an investable commodity futures index intended to reflect the total return from passive, long-only positions, what is the fundamental principle regarding the collateralization of the underlying futures contracts to ensure an unleveraged exposure?

Correct

The question tests the understanding of how commodity futures indices are constructed to represent total return. The key distinction is that these indices are designed to be unleveraged, meaning the full face value of the futures contracts is collateralized by risk-free assets like Treasury bills. This ensures that each dollar invested in the index provides direct exposure to the commodity’s price movements, without the amplified gains or losses that leverage would introduce. Options B, C, and D describe characteristics that are either absent in unleveraged indices (like leverage or active management) or are components of total return but not the defining characteristic of the index’s construction for representing total return in an unleveraged manner.

Incorrect

The question tests the understanding of how commodity futures indices are constructed to represent total return. The key distinction is that these indices are designed to be unleveraged, meaning the full face value of the futures contracts is collateralized by risk-free assets like Treasury bills. This ensures that each dollar invested in the index provides direct exposure to the commodity’s price movements, without the amplified gains or losses that leverage would introduce. Options B, C, and D describe characteristics that are either absent in unleveraged indices (like leverage or active management) or are components of total return but not the defining characteristic of the index’s construction for representing total return in an unleveraged manner.

-

Question 14 of 30

14. Question

When a hedge fund manager decides to broaden their investor base beyond a select group of sophisticated investors and begins to market its investment opportunities more widely, which foundational piece of U.S. securities legislation would most directly dictate the initial registration and disclosure obligations for the fund’s securities?

Correct

This question tests the understanding of how regulatory frameworks, specifically those pertaining to investor protection and disclosure, impact the operational and reporting requirements of alternative investment funds. The CAIA designation emphasizes the importance of understanding these regulatory nuances. Option A is correct because the Securities Act of 1933 primarily governs the initial offering and sale of securities, requiring registration and detailed disclosures to protect investors. Hedge funds, when engaging in public offerings or soliciting investments from a broad range of investors, must comply with these registration and disclosure mandates. Option B is incorrect because while the Investment Advisers Act of 1940 is crucial for registered investment advisers, it doesn’t directly govern the *offering* of securities in the same way the ’33 Act does. Option C is incorrect because the Securities Exchange Act of 1934 primarily deals with the secondary trading of securities and the regulation of exchanges and broker-dealers, not the initial offering. Option D is incorrect because the Commodity Exchange Act (CEA) primarily regulates futures and options markets, which may be relevant to some hedge fund strategies but not the fundamental registration requirements for offering securities.

Incorrect

This question tests the understanding of how regulatory frameworks, specifically those pertaining to investor protection and disclosure, impact the operational and reporting requirements of alternative investment funds. The CAIA designation emphasizes the importance of understanding these regulatory nuances. Option A is correct because the Securities Act of 1933 primarily governs the initial offering and sale of securities, requiring registration and detailed disclosures to protect investors. Hedge funds, when engaging in public offerings or soliciting investments from a broad range of investors, must comply with these registration and disclosure mandates. Option B is incorrect because while the Investment Advisers Act of 1940 is crucial for registered investment advisers, it doesn’t directly govern the *offering* of securities in the same way the ’33 Act does. Option C is incorrect because the Securities Exchange Act of 1934 primarily deals with the secondary trading of securities and the regulation of exchanges and broker-dealers, not the initial offering. Option D is incorrect because the Commodity Exchange Act (CEA) primarily regulates futures and options markets, which may be relevant to some hedge fund strategies but not the fundamental registration requirements for offering securities.

-

Question 15 of 30

15. Question

When analyzing the return characteristics of commodities within a diversified portfolio, which of the following statements best reflects their typical behavior and relationship with financial markets, as suggested by the provided context?

Correct

The provided text highlights that commodity prices are often positively skewed due to supply-side shocks (e.g., OPEC agreements, weather events, political instability) that tend to reduce supply and thus increase prices. These supply disruptions are generally uncorrelated across different commodity markets. Furthermore, these supply shocks negatively impact financial asset prices because higher input costs reduce expected returns for businesses. Therefore, commodities are expected to have a negative correlation with financial markets, not a positive one. The text explicitly states that shocks to commodity markets are expected to be at least uncorrelated with financial markets, and more likely to be negatively correlated.

Incorrect

The provided text highlights that commodity prices are often positively skewed due to supply-side shocks (e.g., OPEC agreements, weather events, political instability) that tend to reduce supply and thus increase prices. These supply disruptions are generally uncorrelated across different commodity markets. Furthermore, these supply shocks negatively impact financial asset prices because higher input costs reduce expected returns for businesses. Therefore, commodities are expected to have a negative correlation with financial markets, not a positive one. The text explicitly states that shocks to commodity markets are expected to be at least uncorrelated with financial markets, and more likely to be negatively correlated.

-

Question 16 of 30

16. Question

A hedge fund manager observes that the implied volatility of a call option on a technology stock is 35%, while the historical volatility of the same stock over the option’s life has been 25%. The manager also notes that similar options on the same stock imply a volatility of 33%. Based on the principles of relative value arbitrage, what action would the manager most likely consider to capitalize on this situation, assuming a mean reversion model is employed?

Correct

Volatility arbitrage, as described, involves comparing the implied volatility of options to their historical volatility or to the implied volatility of other options on the same underlying asset. The core principle is to identify mispriced options based on their volatility. A mean reversion model assumes that implied volatility will revert to its historical average. If implied volatility is significantly higher than historical volatility, the model suggests the option is ‘rich’ (overpriced) and should be sold. Conversely, if implied volatility is lower than historical volatility, the option is considered ‘cheap’ (underpriced) and should be bought. GARCH models forecast future volatility based on past realized volatility and compare this forecast to the implied volatility. The goal in both approaches is to profit from the convergence of implied and expected future volatility.

Incorrect

Volatility arbitrage, as described, involves comparing the implied volatility of options to their historical volatility or to the implied volatility of other options on the same underlying asset. The core principle is to identify mispriced options based on their volatility. A mean reversion model assumes that implied volatility will revert to its historical average. If implied volatility is significantly higher than historical volatility, the model suggests the option is ‘rich’ (overpriced) and should be sold. Conversely, if implied volatility is lower than historical volatility, the option is considered ‘cheap’ (underpriced) and should be bought. GARCH models forecast future volatility based on past realized volatility and compare this forecast to the implied volatility. The goal in both approaches is to profit from the convergence of implied and expected future volatility.

-

Question 17 of 30

17. Question

When analyzing the asset allocation results presented for various hedge fund indices across different levels of investor risk aversion, what is the consistent trend observed regarding the proportion allocated to hedge funds as risk aversion escalates from low to high?

Correct

The provided exhibit demonstrates how an investor’s risk aversion influences asset allocation. At low risk aversion, the model suggests a 100% allocation to hedge funds, indicating a strong preference for return maximization. As risk aversion increases to moderate and then high levels, the allocation to hedge funds significantly decreases, with a corresponding increase in allocations to traditional assets like Treasury bills and bonds. This shift occurs because higher risk aversion prioritizes risk reduction, and diversification across less correlated assets (including traditional ones) helps dampen portfolio volatility. The high allocation to one-year Treasury bills (0.85 or 0.89) in the high risk aversion scenario for several indices, coupled with a near-zero allocation to hedge funds, clearly illustrates this principle. The question asks about the implication of increasing risk aversion on hedge fund allocation, and the data consistently shows a decline, particularly when moving from low to high risk aversion.

Incorrect

The provided exhibit demonstrates how an investor’s risk aversion influences asset allocation. At low risk aversion, the model suggests a 100% allocation to hedge funds, indicating a strong preference for return maximization. As risk aversion increases to moderate and then high levels, the allocation to hedge funds significantly decreases, with a corresponding increase in allocations to traditional assets like Treasury bills and bonds. This shift occurs because higher risk aversion prioritizes risk reduction, and diversification across less correlated assets (including traditional ones) helps dampen portfolio volatility. The high allocation to one-year Treasury bills (0.85 or 0.89) in the high risk aversion scenario for several indices, coupled with a near-zero allocation to hedge funds, clearly illustrates this principle. The question asks about the implication of increasing risk aversion on hedge fund allocation, and the data consistently shows a decline, particularly when moving from low to high risk aversion.

-

Question 18 of 30

18. Question

During a comprehensive review of a company’s funding trajectory, a venture capital firm is evaluating an investment in a firm that has successfully completed beta testing for its product and is now demonstrating initial sales. The company’s primary focus is on scaling its manufacturing capabilities and solidifying its distribution channels. What is the most accurate description of this company’s financial and operational stage, and its typical objective at this juncture?

Correct

The question tests the understanding of the typical financial goals and operational characteristics of a company seeking early-stage venture capital. Early-stage financing is generally used to scale manufacturing, refine business and marketing plans, and establish initial sales. The primary financial objective at this stage is to achieve market penetration and reach the break-even point. While profitability might be on the horizon, it’s not the primary focus or achievement at this stage; rather, it’s the demonstration of commercial viability and the groundwork for future profitability. Managing accounts receivable and preparing for an IPO are more characteristic of later stages like mezzanine financing.

Incorrect

The question tests the understanding of the typical financial goals and operational characteristics of a company seeking early-stage venture capital. Early-stage financing is generally used to scale manufacturing, refine business and marketing plans, and establish initial sales. The primary financial objective at this stage is to achieve market penetration and reach the break-even point. While profitability might be on the horizon, it’s not the primary focus or achievement at this stage; rather, it’s the demonstration of commercial viability and the groundwork for future profitability. Managing accounts receivable and preparing for an IPO are more characteristic of later stages like mezzanine financing.

-

Question 19 of 30

19. Question

When structuring a Leveraged Buyout (LBO) fund, a critical regulatory consideration is to avoid classification as an investment company under the Investment Company Act of 1940. Which of the following strategies is commonly employed by LBO funds to achieve this regulatory status?

Correct

The question tests the understanding of how LBO funds are structured and regulated, specifically their reliance on exemptions from the Investment Company Act of 1940. The text explicitly states that LBO funds utilize provisions like 3(c)(1) and 3(c)(7) to avoid being classified as investment companies. These exemptions are crucial for their operational flexibility and are a common regulatory consideration for such funds, similar to hedge funds. Option B is incorrect because while advisory boards exist, their primary role is not regulatory compliance. Option C is incorrect as the management fee structure, while discussed, is not the primary mechanism for regulatory avoidance. Option D is incorrect because while LBO funds are typically limited partnerships, this structure itself doesn’t exempt them from the Investment Company Act of 1940; specific provisions are needed.

Incorrect

The question tests the understanding of how LBO funds are structured and regulated, specifically their reliance on exemptions from the Investment Company Act of 1940. The text explicitly states that LBO funds utilize provisions like 3(c)(1) and 3(c)(7) to avoid being classified as investment companies. These exemptions are crucial for their operational flexibility and are a common regulatory consideration for such funds, similar to hedge funds. Option B is incorrect because while advisory boards exist, their primary role is not regulatory compliance. Option C is incorrect as the management fee structure, while discussed, is not the primary mechanism for regulatory avoidance. Option D is incorrect because while LBO funds are typically limited partnerships, this structure itself doesn’t exempt them from the Investment Company Act of 1940; specific provisions are needed.

-

Question 20 of 30

20. Question

During the annual rebalancing of the Dow Jones-AIG Commodity Index (DJ-AIGCI), an analyst observes that the weight of a particular agricultural commodity has decreased to 1.8% due to significant price depreciation over the past year. According to the index’s established diversification rules, what action must be taken regarding this commodity?

Correct

The Dow Jones-AIG Commodity Index (DJ-AIGCI) employs specific rules to manage its composition and prevent over-concentration in any single commodity or sector. One of these rules dictates that no single commodity can represent less than 2% of the index’s total weight. This ensures a baseline level of diversification across all included commodities. The scenario describes a situation where a commodity’s weight has fallen below this threshold, necessitating an adjustment to maintain compliance with the index’s structural integrity. Therefore, the index manager would need to increase the allocation to this underweighted commodity to meet the minimum 2% requirement.

Incorrect

The Dow Jones-AIG Commodity Index (DJ-AIGCI) employs specific rules to manage its composition and prevent over-concentration in any single commodity or sector. One of these rules dictates that no single commodity can represent less than 2% of the index’s total weight. This ensures a baseline level of diversification across all included commodities. The scenario describes a situation where a commodity’s weight has fallen below this threshold, necessitating an adjustment to maintain compliance with the index’s structural integrity. Therefore, the index manager would need to increase the allocation to this underweighted commodity to meet the minimum 2% requirement.

-

Question 21 of 30

21. Question

A hedge fund manager, recently having obtained their Chartered Alternative Investment Analyst (CAIA) designation, is discussing their strategy with potential investors. They express confidence in their short-selling capabilities, stating, ‘I haven’t shorted before, but I do have my CAIA.’ Which of the following best describes the potential disconnect between the manager’s statement and the realities of short selling, as understood within the alternative investment industry?

Correct

The CAIA designation signifies a commitment to understanding alternative investments, including the complexities of short selling. However, the quote highlights that possessing the designation alone does not equate to practical expertise in short selling. Short selling involves unique risks such as unlimited potential loss and the phenomena of beta expansion and short squeezes, which are distinct from traditional long-only investing. Furthermore, successful short selling requires specialized knowledge of prime brokerage relationships, collateral borrowing, and rebate negotiation. Therefore, while the CAIA is valuable, it is not a direct substitute for the hands-on skills and experience necessary for effective short selling.

Incorrect

The CAIA designation signifies a commitment to understanding alternative investments, including the complexities of short selling. However, the quote highlights that possessing the designation alone does not equate to practical expertise in short selling. Short selling involves unique risks such as unlimited potential loss and the phenomena of beta expansion and short squeezes, which are distinct from traditional long-only investing. Furthermore, successful short selling requires specialized knowledge of prime brokerage relationships, collateral borrowing, and rebate negotiation. Therefore, while the CAIA is valuable, it is not a direct substitute for the hands-on skills and experience necessary for effective short selling.

-

Question 22 of 30

22. Question

During a comprehensive review of historical market data, an analyst observes a period characterized by widespread corporate malfeasance and a significant erosion of investor confidence in financial reporting. According to the principles of equity risk premium estimation, how would this environment likely impact the required compensation for holding equities relative to risk-free assets?

Correct

The question tests the understanding of how market events influence the equity risk premium (ERP). The provided text highlights that periods of significant market turmoil, such as accounting scandals (like Enron and WorldCom), lead to increased investor uncertainty and a higher demand for compensation to hold risky assets. This increased demand translates directly into a higher ERP. The tech bubble and portfolio insurance events, while significant, are presented as periods where the ERP approached zero, indicating a mispricing or perception of risk, which was subsequently corrected. Therefore, accounting scandals are directly linked to a substantial increase in the ERP.

Incorrect

The question tests the understanding of how market events influence the equity risk premium (ERP). The provided text highlights that periods of significant market turmoil, such as accounting scandals (like Enron and WorldCom), lead to increased investor uncertainty and a higher demand for compensation to hold risky assets. This increased demand translates directly into a higher ERP. The tech bubble and portfolio insurance events, while significant, are presented as periods where the ERP approached zero, indicating a mispricing or perception of risk, which was subsequently corrected. Therefore, accounting scandals are directly linked to a substantial increase in the ERP.

-

Question 23 of 30

23. Question

When establishing a new alternative investment fund, a manager is meticulously reviewing the regulatory requirements to ensure compliance and protect investors. Which of the following regulatory principles is most directly aimed at preventing the fund from being used for illicit financial activities and ensuring that only suitable investors are onboarded?

Correct

This question tests the understanding of how regulatory frameworks, specifically those pertaining to investor protection and market integrity, influence the operational and disclosure requirements for alternative investment managers. The CAIA designation emphasizes the importance of understanding these regulatory landscapes. Option A is correct because the “Know Your Customer” (KYC) and Anti-Money Laundering (AML) regulations are fundamental to preventing illicit financial activities and ensuring that investors are properly vetted, which is a core tenet of responsible financial management and regulatory compliance. Option B is incorrect because while due diligence is crucial, it’s a broader concept that encompasses more than just regulatory adherence; it includes assessing the investment strategy, team, and operational risks. Option C is incorrect because while performance reporting is important, it’s a separate regulatory and ethical obligation from the foundational KYC/AML requirements. Option D is incorrect because capital adequacy rules are primarily focused on the financial stability of the firm itself, not directly on the vetting of individual investors, although they are part of the overall regulatory environment.

Incorrect

This question tests the understanding of how regulatory frameworks, specifically those pertaining to investor protection and market integrity, influence the operational and disclosure requirements for alternative investment managers. The CAIA designation emphasizes the importance of understanding these regulatory landscapes. Option A is correct because the “Know Your Customer” (KYC) and Anti-Money Laundering (AML) regulations are fundamental to preventing illicit financial activities and ensuring that investors are properly vetted, which is a core tenet of responsible financial management and regulatory compliance. Option B is incorrect because while due diligence is crucial, it’s a broader concept that encompasses more than just regulatory adherence; it includes assessing the investment strategy, team, and operational risks. Option C is incorrect because while performance reporting is important, it’s a separate regulatory and ethical obligation from the foundational KYC/AML requirements. Option D is incorrect because capital adequacy rules are primarily focused on the financial stability of the firm itself, not directly on the vetting of individual investors, although they are part of the overall regulatory environment.

-

Question 24 of 30

24. Question

When analyzing the return distribution of an alternative investment strategy, a financial analyst observes that the average return is significantly lower than the median return. Based on the principles of statistical moments, what characteristic is most likely present in this return distribution?

Correct

The question tests the understanding of how skewness impacts the relationship between the mean and median of a return distribution. A negatively skewed distribution, as described in the provided text, has a tail extending towards lower returns. This means that extreme negative returns pull the mean down, making it lower than the median, which represents the midpoint of the data. Therefore, a negative skew implies the mean is less than the median.

Incorrect

The question tests the understanding of how skewness impacts the relationship between the mean and median of a return distribution. A negatively skewed distribution, as described in the provided text, has a tail extending towards lower returns. This means that extreme negative returns pull the mean down, making it lower than the median, which represents the midpoint of the data. Therefore, a negative skew implies the mean is less than the median.

-

Question 25 of 30

25. Question

During the due diligence process for a hedge fund, an investor discovers that the manager also operates several separate accounts for high-net-worth individuals, employing the same investment strategy. The investor is concerned about potential conflicts of interest regarding the allocation of proprietary trade ideas. Which of the following actions is most crucial for the investor to undertake to mitigate this risk?

Correct

The scenario highlights a critical aspect of hedge fund due diligence: ensuring fair allocation of investment opportunities. When a hedge fund manager manages both a hedge fund and separate accounts for individual clients, there’s a potential for conflicts of interest. The manager might prioritize opportunities for one over the other, or allocate trades in a way that benefits themselves or certain clients disproportionately. Prime brokers and custodians typically do not monitor the fairness of trade allocations. Therefore, it is the investor’s responsibility to verify that trade ideas are distributed equitably between the hedge fund and any separate accounts managed by the same manager. This ensures that all clients receive a fair share of potentially profitable strategies, aligning with the principle of fiduciary duty.

Incorrect

The scenario highlights a critical aspect of hedge fund due diligence: ensuring fair allocation of investment opportunities. When a hedge fund manager manages both a hedge fund and separate accounts for individual clients, there’s a potential for conflicts of interest. The manager might prioritize opportunities for one over the other, or allocate trades in a way that benefits themselves or certain clients disproportionately. Prime brokers and custodians typically do not monitor the fairness of trade allocations. Therefore, it is the investor’s responsibility to verify that trade ideas are distributed equitably between the hedge fund and any separate accounts managed by the same manager. This ensures that all clients receive a fair share of potentially profitable strategies, aligning with the principle of fiduciary duty.

-

Question 26 of 30

26. Question

A portfolio manager is analyzing a six-month futures contract on the Euro/USD exchange rate. The current spot rate is $1.10 per Euro. The prevailing risk-free interest rate in the United States is 5% per annum, and the risk-free interest rate in the Eurozone is 3% per annum. To prevent arbitrage opportunities, what should be the approximate price of this futures contract?

Correct

The question tests the understanding of the interest rate parity theorem as applied to currency futures pricing. The core principle is that the futures price of a foreign currency should reflect the spot exchange rate adjusted for the interest rate differential between the two countries. The formula F = S * e^((r – f) * (T – t)) encapsulates this. In this scenario, the domestic risk-free rate (r) is 5%, the foreign risk-free rate (f) for the Euro is 3%, the spot rate (S) is $1.10 per Euro, and the time to maturity (T-t) is 0.5 years. Plugging these values into the formula: F = 1.10 * e^((0.05 – 0.03) * 0.5) = 1.10 * e^(0.02 * 0.5) = 1.10 * e^(0.01) \approx 1.10 * 1.01005 = 1.111055. Therefore, the futures price should be approximately $1.1111 per Euro to prevent arbitrage. Option B ($1.1055) would imply a smaller interest rate differential or shorter time period. Option C ($1.1221) would suggest a higher interest rate differential or longer time period. Option D ($1.0946) would indicate the domestic rate being lower than the foreign rate, which is contrary to the given information.

Incorrect

The question tests the understanding of the interest rate parity theorem as applied to currency futures pricing. The core principle is that the futures price of a foreign currency should reflect the spot exchange rate adjusted for the interest rate differential between the two countries. The formula F = S * e^((r – f) * (T – t)) encapsulates this. In this scenario, the domestic risk-free rate (r) is 5%, the foreign risk-free rate (f) for the Euro is 3%, the spot rate (S) is $1.10 per Euro, and the time to maturity (T-t) is 0.5 years. Plugging these values into the formula: F = 1.10 * e^((0.05 – 0.03) * 0.5) = 1.10 * e^(0.02 * 0.5) = 1.10 * e^(0.01) \approx 1.10 * 1.01005 = 1.111055. Therefore, the futures price should be approximately $1.1111 per Euro to prevent arbitrage. Option B ($1.1055) would imply a smaller interest rate differential or shorter time period. Option C ($1.1221) would suggest a higher interest rate differential or longer time period. Option D ($1.0946) would indicate the domestic rate being lower than the foreign rate, which is contrary to the given information.

-

Question 27 of 30

27. Question

When evaluating an investment in a hedge fund, an investor identifies a risk that is specific to the manager’s internal operational procedures and the unique skills employed, rather than being tied to broader market movements or asset class characteristics. According to principles discussed in hedge fund risk management, how should this type of risk be categorized?

Correct

The question probes the understanding of process risk in the context of hedge funds, as distinct from fundamental economic risks. Process risk is defined as idiosyncratic risk stemming from the manager’s operational structure and execution, which investors generally prefer not to bear. The provided text highlights that this type of risk is inherent to the skill-based nature of the hedge fund industry. Diversification across hedge fund styles or investing in funds of funds is presented as a strategy to mitigate this risk, analogous to how Modern Portfolio Theory (MPT) suggests diversifying stock portfolios to reduce idiosyncratic risk. Therefore, process risk is not a fundamental economic risk that investors seek compensation for, but rather an operational inefficiency or unique characteristic of a specific manager.

Incorrect

The question probes the understanding of process risk in the context of hedge funds, as distinct from fundamental economic risks. Process risk is defined as idiosyncratic risk stemming from the manager’s operational structure and execution, which investors generally prefer not to bear. The provided text highlights that this type of risk is inherent to the skill-based nature of the hedge fund industry. Diversification across hedge fund styles or investing in funds of funds is presented as a strategy to mitigate this risk, analogous to how Modern Portfolio Theory (MPT) suggests diversifying stock portfolios to reduce idiosyncratic risk. Therefore, process risk is not a fundamental economic risk that investors seek compensation for, but rather an operational inefficiency or unique characteristic of a specific manager.

-

Question 28 of 30

28. Question

A hedge fund manager observes the following for the USD/JPY currency pair: Current spot rate (JPY/USD) = 100; U.S. risk-free rate = 6% per annum; Japanese risk-free rate = 1% per annum; Time to maturity for a futures contract = 3 months. If the futures contract price were such that it allowed for a risk-free profit by borrowing yen, converting to dollars, investing in U.S. dollar assets, and then repaying the yen loan using the proceeds converted back at the futures rate, what should the futures price (in USD per JPY) be to eliminate this arbitrage opportunity, assuming the interest rate parity theorem holds?

Correct

The question tests the understanding of the interest rate parity theorem as applied to currency futures pricing. The core of the theorem is that the difference in interest rates between two countries should be reflected in the forward or futures exchange rate. Specifically, the futures price (F) should be such that it eliminates arbitrage opportunities. The formula for currency futures pricing, incorporating interest rate differentials, is F = S * e^((r – f) * (T – t)), where S is the spot rate, r is the domestic risk-free rate, f is the foreign risk-free rate, and (T – t) is the time to maturity. In this scenario, the U.S. is the domestic country (r = 6%) and Japan is the foreign country (f = 1%). The spot rate is 100 JPY/USD, which is equivalent to $0.01 USD/JPY. The time to maturity is three months, or 0.25 years. Plugging these values into the formula: F = 0.01 * e^((0.06 – 0.01) * 0.25) = 0.01 * e^(0.05 * 0.25) = 0.01 * e^0.0125. Calculating e^0.0125 gives approximately 1.012578. Therefore, F = 0.01 * 1.012578 = 0.01012578 USD/JPY. This translates to approximately 98.76 JPY/USD. The scenario describes a situation where the futures price is not aligned with this parity, creating an arbitrage opportunity. The hedge fund manager borrows yen, converts to dollars, invests dollars at the U.S. rate, and uses the proceeds to repay the yen loan. The arbitrage profit arises from the difference between the dollar investment return and the cost of repaying the yen loan, adjusted by the exchange rate. The question asks for the futures price that would prevent such arbitrage, which is precisely the price dictated by the interest rate parity theorem.

Incorrect

The question tests the understanding of the interest rate parity theorem as applied to currency futures pricing. The core of the theorem is that the difference in interest rates between two countries should be reflected in the forward or futures exchange rate. Specifically, the futures price (F) should be such that it eliminates arbitrage opportunities. The formula for currency futures pricing, incorporating interest rate differentials, is F = S * e^((r – f) * (T – t)), where S is the spot rate, r is the domestic risk-free rate, f is the foreign risk-free rate, and (T – t) is the time to maturity. In this scenario, the U.S. is the domestic country (r = 6%) and Japan is the foreign country (f = 1%). The spot rate is 100 JPY/USD, which is equivalent to $0.01 USD/JPY. The time to maturity is three months, or 0.25 years. Plugging these values into the formula: F = 0.01 * e^((0.06 – 0.01) * 0.25) = 0.01 * e^(0.05 * 0.25) = 0.01 * e^0.0125. Calculating e^0.0125 gives approximately 1.012578. Therefore, F = 0.01 * 1.012578 = 0.01012578 USD/JPY. This translates to approximately 98.76 JPY/USD. The scenario describes a situation where the futures price is not aligned with this parity, creating an arbitrage opportunity. The hedge fund manager borrows yen, converts to dollars, invests dollars at the U.S. rate, and uses the proceeds to repay the yen loan. The arbitrage profit arises from the difference between the dollar investment return and the cost of repaying the yen loan, adjusted by the exchange rate. The question asks for the futures price that would prevent such arbitrage, which is precisely the price dictated by the interest rate parity theorem.

-

Question 29 of 30

29. Question

When analyzing investment products that aim to outperform a specific market index through active management, but still maintain a substantial correlation with that index, which segment of the ‘beta continuum’ best describes such strategies, considering they exhibit a linear relationship with the benchmark but with less pronounced linearity than pure beta exposures?

Correct

The question probes the understanding of the ‘beta continuum’ as presented in the CAIA curriculum. Bulk beta products, like the active equity product benchmarked against the S&P 500 in the provided exhibit, are characterized by a significant correlation with their benchmark, indicating substantial exposure to systematic risk. However, they also incorporate active management aimed at generating alpha. The key distinction is that while they exhibit a linear relationship with the benchmark, this linearity is less pronounced than in ‘classic beta’ due to the active risk-taking. The other options represent different points on the beta continuum or related concepts. Classic beta aims to capture broad systematic risk premiums with minimal active risk. Alternative beta seeks systematic risk premiums outside traditional asset classes and often has low correlation to stocks and bonds. Fundamental beta refers to alpha embedded within index construction itself.

Incorrect

The question probes the understanding of the ‘beta continuum’ as presented in the CAIA curriculum. Bulk beta products, like the active equity product benchmarked against the S&P 500 in the provided exhibit, are characterized by a significant correlation with their benchmark, indicating substantial exposure to systematic risk. However, they also incorporate active management aimed at generating alpha. The key distinction is that while they exhibit a linear relationship with the benchmark, this linearity is less pronounced than in ‘classic beta’ due to the active risk-taking. The other options represent different points on the beta continuum or related concepts. Classic beta aims to capture broad systematic risk premiums with minimal active risk. Alternative beta seeks systematic risk premiums outside traditional asset classes and often has low correlation to stocks and bonds. Fundamental beta refers to alpha embedded within index construction itself.

-

Question 30 of 30

30. Question

When implementing a stress test for a diversified investment portfolio comprising stocks, bonds, hedge funds, private equity, commodities, and real estate, which of the following outcomes would most directly indicate a failure of the portfolio’s diversification strategy under adverse market conditions?

Correct

Scenario analysis and stress testing are techniques used to evaluate the impact of extreme or out-of-the-ordinary events on financial instruments or portfolios. The core idea is to assess how a system’s stability holds up when operating outside its normal parameters. In the context of a diversified portfolio, while asset classes may exhibit low correlation over extended periods, during times of market stress, these correlations can converge. This convergence reduces the expected diversification benefits, as multiple asset classes may decline simultaneously. Therefore, stress testing aims to identify potential vulnerabilities arising from such synchronized movements during adverse market conditions, such as the credit and liquidity crisis of 2007, where high-yield bond spreads widened significantly due to a flight to safety and increased perceived risk.

Incorrect

Scenario analysis and stress testing are techniques used to evaluate the impact of extreme or out-of-the-ordinary events on financial instruments or portfolios. The core idea is to assess how a system’s stability holds up when operating outside its normal parameters. In the context of a diversified portfolio, while asset classes may exhibit low correlation over extended periods, during times of market stress, these correlations can converge. This convergence reduces the expected diversification benefits, as multiple asset classes may decline simultaneously. Therefore, stress testing aims to identify potential vulnerabilities arising from such synchronized movements during adverse market conditions, such as the credit and liquidity crisis of 2007, where high-yield bond spreads widened significantly due to a flight to safety and increased perceived risk.